This intel artifact is an attempt to understand the main constraints that dictate the dynamics we’re observing in the telco industry.

The telecom market is trapped in an incentive-structure failure.

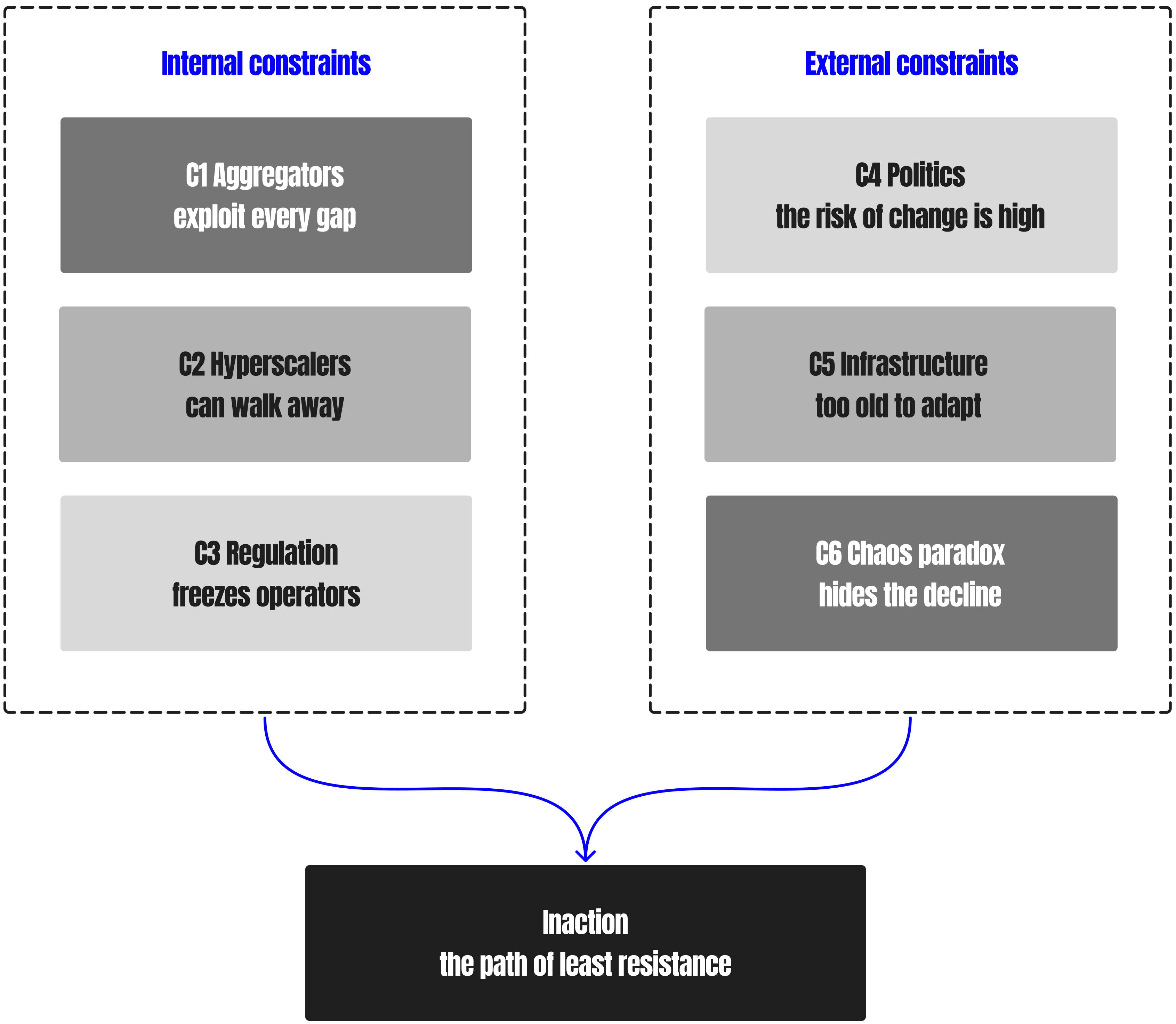

Six constraints interlock to create a system where every actor is stuck: regulators freeze the rules, aggregators exploit the gaps, hyperscalers control the economics, legacy infrastructure can’t adapt, internal politics block change, and, most critically, the chaos itself becomes a reason not to act.

Inflated metrics and dirty data provide political cover that makes the real problem harder to see and harder to fix. These constraints don’t just coexist, but also reinforce each other. This document maps how the trap works.

At its core, the telecom A2P market is suffering from an incentive-structure failure. The industry was built on a model where incentives no longer match reality.

Any solution to this system would have to address both sides of the incentive failure simultaneously, the external distortions and the internal paralysis, without requiring the operator to take on the very CAPEX risk and political exposure that keeps them frozen in the first place.

Aggregators sit between enterprises and operators, and their entire business model is built on exploiting gaps in pricing, visibility, and regulation. They are rewarded for finding the cheapest possible route, even when it violates operator rules.

Why does this happen?

Why does this persist?

How does this trap operators?

The impossible situation:

The largest buyers of A2P SMS, such as Google, Amazon, Apple, can shift their traffic instantly, negotiate globally, and decide whether SMS is “worth it” or not. Operators have zero leverage.

Why does this happen?

Why does this persist?

How does this trap operators?

The impossible situation:

The regulatory frameworks that govern SMS pricing, traffic, and enforcement were designed in the era of P2P messaging. They assume low volume, simple traffic, and predictable patterns, none of which remain true today.

Why does this happen?

Why does this persist?

How does this trap operators?

Operators are forced into:

The impossible situation:

Operators are massive bureaucratic organizations with risk-averse cultures. Any change to core infrastructure requires cross-department alignment, budget requests, procurement cycles, security reviews, and political buy-in.

Why does this happen?

Why does this persist?

How does this trap operators?

The impossible situation:

P2P-era SMSCs, static firewalls, and legacy routing systems were never designed for OTP bursts, fintech flows, AI-driven fraud, or massive enterprise A2P traffic.

Why does this happen?

Why does this persist?

How does this trap operators?

The impossible situation:

The A2P ecosystem is filled with fake volume, bot-driven traffic, spam bursts, fraud loops, and grey-route patterns. Paradoxically, this chaos, apart from hurting operators, it also benefits them on paper. Inflated metrics make the business appear stronger, justify pricing increases, and maintain a weak infrastructure and lack of accountability.

Why does this happen?

Why does this persist?

How does this trap operators?

The impossible situation:

Each player is doing what makes sense from their own position. Aggregators find the cheapest route because that’s how they survive on thin margins. Regulators keep prices low because that’s their mandate. Hyperscalers shift traffic when costs rise because that's basic procurement logic. Internal teams avoid risky upgrades because they get rewarded for stability, not innovation.

Nobody is being stupid or malicious. Everyone is following their own incentives correctly. The problem is that when all of those rational decisions combine, the system they produce is irrational: it traps everyone, including the people making the individually sensible choices.

That’s what makes it an incentive-structure failure rather than a competence failure. The dysfunction isn’t coming from anyone doing the wrong thing, but from the structure that connects all the right things into a deadlock.